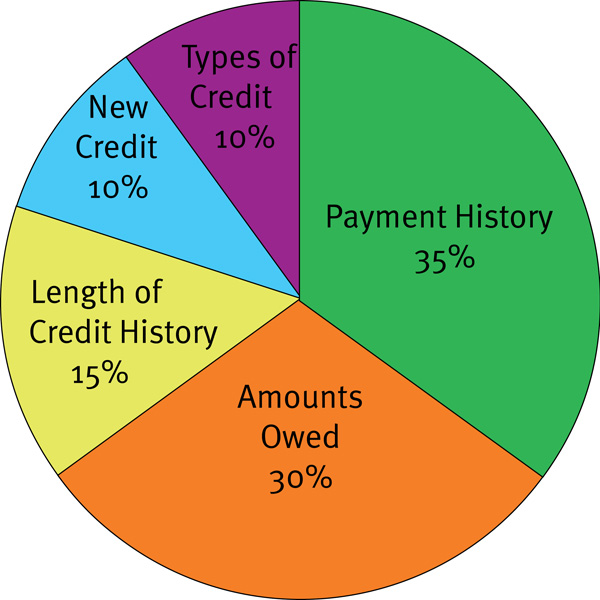

The complete details of the FICO score are not available, but the company provides the general components of a FICO credit score. FICO takes information in your credit report and breaks that information into five categories. These five categories each get different weights as follows…..

1. Payment History–35 Percent of the Total Credit Score

Your payment history or making the repayment of past debt is the most important factor in calculating credit scores. According to FICO, past long-term behavior is used to forecast future long-term behavior.

2. Amount of Debt -30 Percent of the Total Credit Score

Credit cards are a type of revolving credit line in which you can charge (borrow) as much or as little as desired up to a limit. The more debt you have as compared to your credit line, the more of a negative effect there is on your credit score. Experts recommend that the amount owed should not exceed 20 percent of your credit limits. (some say 30%). This 20 or 30 percent rule applies to each individual credit card as well as the overall level of debt. This debt to available credit ratio is called your utilization ratio.

3. Length of Credit History -15 Percent of the Total Credit Score

This aspect of the score is based on the length of time each of your accounts has been open and the length of time since the account’s most recent activity. A longer credit history provides more information and offers a better indicator of your behavior. To improve your credit score, if you don’t have a history, you should begin using credit (think of your college kids), and if you have credit cards, you should try to maintain them for a long period of time. (Unless you play the game and need to cancel your card!!!)

4. New Credit-10 Percent of the Total Credit Score

Even if there are many sign-up bonuses that you would like to take advantage of, try not to open too many credit cards at one time as it could be seen as a sign that you are in financial trouble and need significant access to lots of credit. I usually try to space out my applications to every 4-6 months. My score is good, so I usually do not have a problem following this guideline. However, for example, Chase is hesitant to approve you for new cards within 6 months of getting another Chase card. If you really want another Chase card, I suggest you call their credit reallocation line and just move some of your existing credit to the new card that you want to get. I have done this in the past, Rob has too, and we have both been very successful. I have also done this with Citibank and Barclays with success. You can access a list of phone numbers to call to reallocate your credit in this post.

Do credit inquires affect your credit score?

For the most part, credit inquiries have an impact on your score, but a small one. They may affect your score more if you don’t have many accounts or you have a short credit history. Remember, don’t apply for too many at once as large numbers of inquiries could signify greater risk to the FICO and the other companies that calculate credit score.

5. Credit Mix -10 Percent of the Total Credit Score

Experts say that repaying a variety of debt helps increase your credit score. Besides revolving credit, other debt that helps includes installment loans. Installment loans are a set loan amount up front (not revolving) that you pay off in installments.